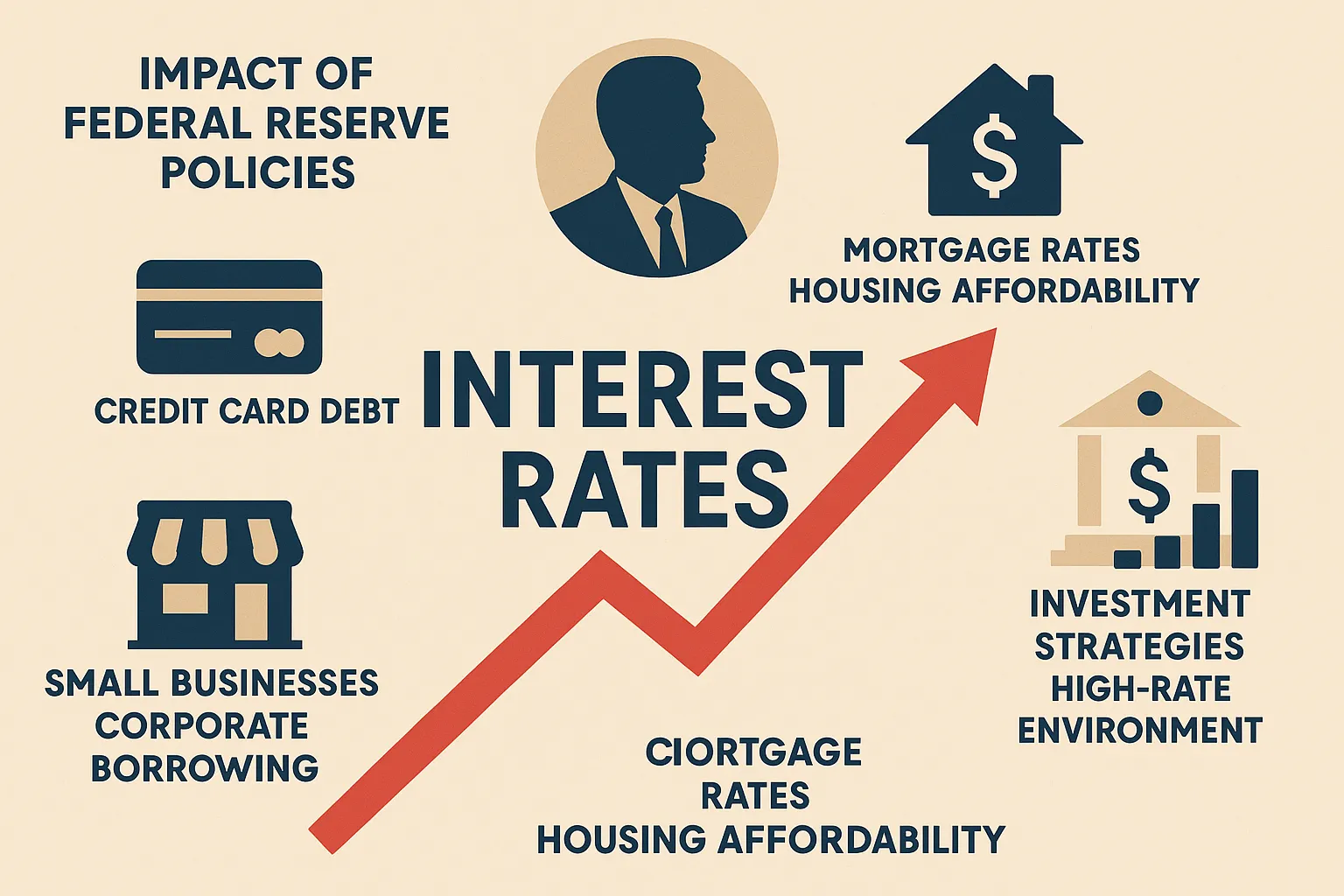

How the Federal Reserve’s Interest Rate Decisions Are Reshaping the U.S. Financial Landscape in 2025

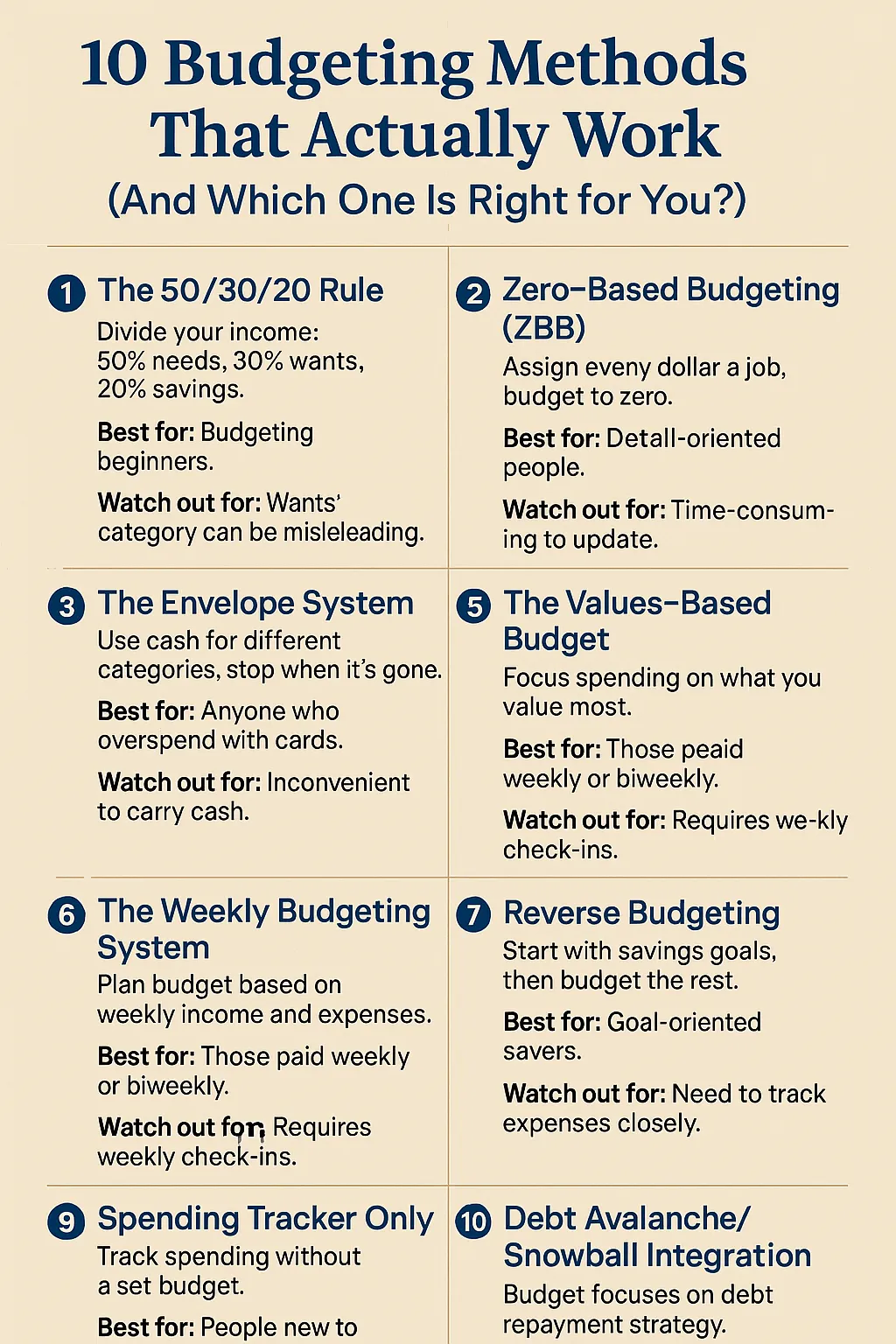

Managing money without a plan is like trying to navigate a road trip without a map. That’s where budgeting comes in. But not every budgeting method works for every person. Some people thrive with strict systems; others need more flexibility. The key is finding a method that aligns with your habits and goals. In this article, we’ll explore ten proven budgeting strategies—each with its pros, cons, and ideal user type.

How it works:

You divide your after-tax income into three categories:

Why it works:

It’s simple, intuitive, and doesn’t require tracking every expense.

Best for:

Budgeting beginners who want an easy-to-follow structure without micromanagement.

Watch out for:

The 30% “wants” category can be misleading if your “needs” already take up more than 50%.

How it works:

Every dollar you earn is assigned a job—whether it’s paying bills, saving, or investing. At the end, your budget should “zero out.”

Why it works:

It forces full awareness of where your money goes and helps eliminate wasteful spending.

Best for:

Detail-oriented people or those trying to aggressively pay off debt.

Watch out for:

Time-consuming. It requires updating your budget frequently—ideally every month.

How it works:

You allocate cash into physical envelopes for different categories (e.g., groceries, gas, entertainment). Once the money’s gone, you stop spending.

Why it works:

It builds discipline and avoids overspending.

Best for:

People who overspend with debit/credit cards and want to stick to a hard limit.

Watch out for:

Carrying cash isn’t convenient or secure for everyone. Some use digital envelope apps like Goodbudget as an alternative.

How it works:

You automatically transfer a set portion of your income into savings/investments before spending anything else. Whatever’s left is what you live on.

Why it works:

Saves money automatically, builds wealth faster.

Best for:

Anyone struggling to save consistently or who tends to “save what’s left”—and ends up saving nothing.

Watch out for:

You still need a rough budget to make sure expenses don’t exceed the leftover amount.

How it works:

You build your budget around your core values. Spend less on things you don’t care about (e.g., cable TV) and more on what brings you joy (e.g., travel, education).

Why it works:

Creates a more meaningful and sustainable financial lifestyle.

Best for:

People tired of rigid systems who want a purpose-driven approach to money.

Watch out for:

Can be subjective. Requires deep honesty and self-reflection to avoid rationalizing indulgent purchases.

How it works:

Rather than planning for the whole month, you budget weekly based on your income and expenses. This helps break large goals into smaller, manageable chunks.

Why it works:

Keeps you constantly aware of your spending, especially if you get paid weekly or biweekly.

Best for:

Those who feel overwhelmed by monthly planning or frequently overspend early in the month.

Watch out for:

It requires weekly check-ins and can feel repetitive to some users.

Here are 4 other notable strategies:

There’s no “best” budgeting method—only what works for your lifestyle and goals. Some people succeed with structure; others prefer freedom with boundaries.

If you’re just starting out, try the 50/30/20 rule for a few months. Then, evolve into more detailed systems like zero-based budgeting or pay-yourself-first as you gain confidence.

{kind=link}